About MONEYME

Credit Score Tool

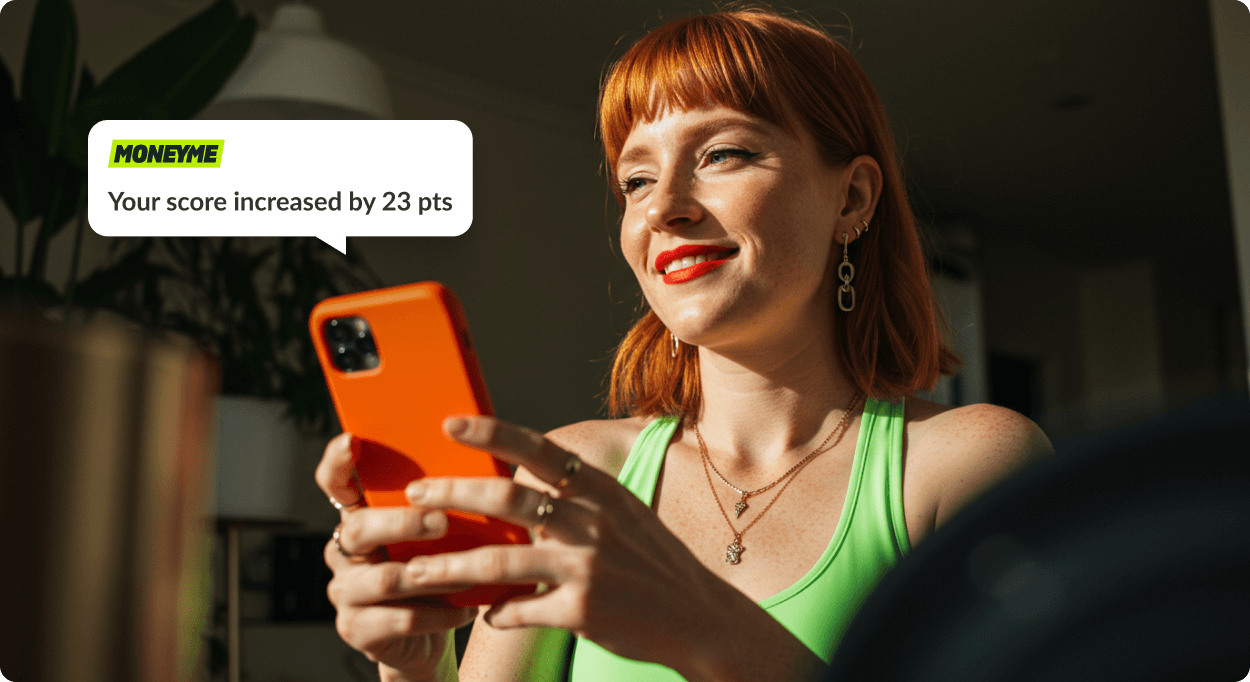

Banks know your credit score... do you?

Track your score for free and learn how to improve it.

Won't impact your credit score!

Understand how lenders see you

When applying for loans and credit, your credit score can affect your approval chances and the interest rate you're offered.

Check your score in the MONEYME app!

Subject to lender criteria and T&Cs

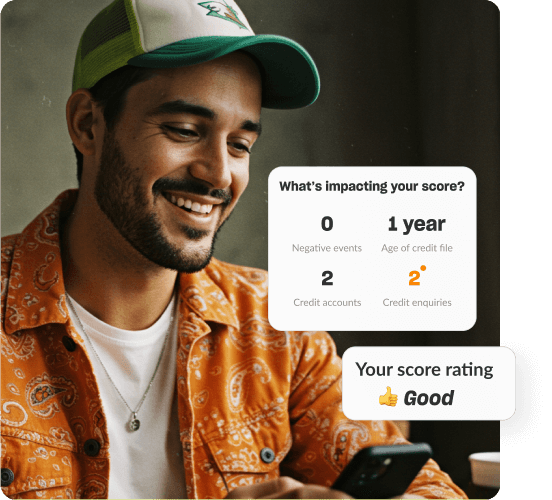

Get in-depth insights

See what's on your credit file, how it's impacting your score and what you can do about it.

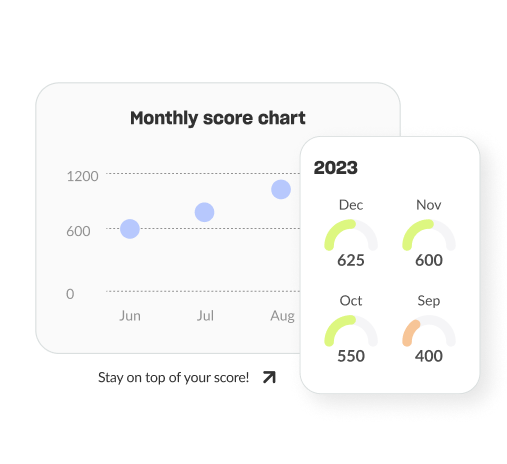

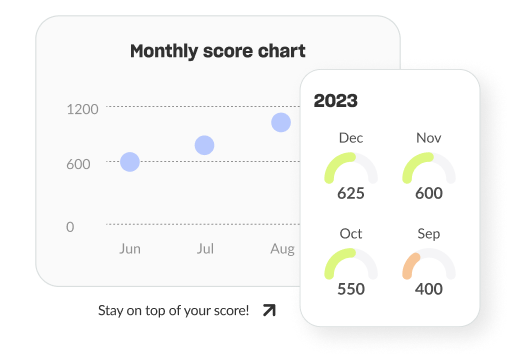

Track your progress

We keep track of your score history so you can see how your score changes over time. Watch it improve or spot when something has impacted it negatively.

Boost your knowledge

Learn all there is to know about credit scores. We share useful tips and tricks on how to boost your score, how to avoid the common mistakes that will tank it, and much more.

Check your credit score

The MONEYME app provides a fast and easy way to check your credit score in Australia, and it's completely free. Simply download the app, access your credit score and receive personalised insights to understand the factors that influence it.

Understanding how credit scores work in Australia

Your credit score reflects your past credit use, repayment history, and the credit accounts you currently have. Late or missed payments can lower your score, while a history of consistent, timely repayments can increase your score over time. In simple terms, a high credit score demonstrates your trustworthiness to lenders and can help you access better loan terms and a lower interest rate.

Benefits of monitoring your credit score

Here's how checking your credit score can help you take control of your finances:

- Understand your score: Getting to know your credit score helps you make smart decisions about loans, credit cards, and how you spend your money.

- Get better deals: Improving your credit score can help you get a better deal with lenders, like lower interest rates on loans, giving you more money in your pocket!

- Track your success: Watch your credit score rise as you improve your credit habits, and celebrate your achievements as you build a stronger financial future.

- Fraud protection: By keeping an eye on your credit score, you can spot any unauthorised activity right away and take action to protect yourself.

- Peace of mind: By understanding and improving your score, you're setting yourself up for better financial outcomes in the future, whether it's buying a home or starting a business.

With no impact to your credit score

Award-winning lender

We’re trusted by over 110,000 Aussies

MONEYME Reviews Average rating: 4.7, based on 4700 reviewsWill definitely be recommending MONEYME to friends and family!

Quick and efficient service, will definitely be recommending MONEYME to friends and family!

JackOct 15, 2025

Quick, easy and hassle free!

Quick, easy and hassle free! I was pleasantly surprised how easy the process was. Also being able to make extra repayments and payout the loan early without penalty, is a big bonus. Recommended!

LindaSep 27, 2025

Easy to deal with.

Easy to deal with and open about the odds and ends of the deal on the purchase. I will continue using MONEYME for any future purchases for the simple reason of not having to deal with all the issues the big banks have with a purchase. Great work Eujin.

LeslieSept 26, 2025

Super fast and easy application.

Excellent Customers service, super fast and easy application with the response within hrs.

ConsumerSep 18, 2025

Approval was fast and even the car dealership was blown away.

Approval was fast and even the car dealership was blown away by the speed and ease of dealing with MONEYME. I had my new car in no time! Highly recommend!

NicholeSep 13, 2025

MONEYME is one of the best finance companies I've ever gone through.

MONEYME is one of the best finance companies I've ever gone through great people and what a fantastic service they provide. MONEYME definitely goes above and beyond to satisfy their customers, thank you so much I would highly recommend MONEYME to anyone Australia wide.

TrinitySep 10, 2025

Great rate and helpful people making this purchase smooth and easy.

A fantastic experience of getting the right finance for my new vehicle. No fuss, no problems, a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

ShazJuly 10, 2025

Very Happy!! MONEYME finance was so easy to work with.

They made the whole experience from start to finish stress free and simple for me to understand which was exactly what I needed. They were just so quick and efficient, the only waiting was with the car yard itself. I would use MONEYME again. I highly recommend them to anyone wanting quick approval at a great rate with fantastic service.

BrookeMay 23, 2025

Overall great experience.

Super quick approval and great interest rate. Money was in the bank within minutes of me accepting the offer. Overall great experience.

JodieMay 9, 2025

Very easy, seamless process.

Every part of the way i had ongoing communication and I knew where I was at every stage. I was able to sign all documents online. The contract was easy to read and understand. The app is very easy to navigate with a easy to find phone number if i ever need assistance.

KerrinMay 21, 2025

Quick and easy to apply.

Great interest compared to other loans. No hidden costs. Fast and efficient.

RenayMar 7, 2025

A fantastic experience for getting the right finance from my new vehicle.

No fuss, no problems a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

ShazJun 8, 2025

Easiest process.

MONEYME has been so easy to navigate the website and the app, always in contact every step of the application. They gave me a chance to get my family a new car. Great company, fair prices, 100%

JadeJan 13, 2025

Great for debt consolidation!

I have used MONEYME a few times as they are simple and efficient. Response time is super quick and the rates are competitive. I was on a crazy rate with a credit card company and used MONEYME to consolidate that debt and reduce my repayments.

ECJan 6, 2025

Professional fast service.

We had a wonderful experience with MONEYME, fast service and very professional, we will definitely be using them again!

BiancaJan 03, 2025

Will definitely be recommending MONEYME to friends and family!

Quick and efficient service, will definitely be recommending MONEYME to friends and family!

JackOct 15, 2025

Quick, easy and hassle free!

Quick, easy and hassle free! I was pleasantly surprised how easy the process was. Also being able to make extra repayments and payout the loan early without penalty, is a big bonus. Recommended!

LindaSep 27, 2025

Easy to deal with.

Easy to deal with and open about the odds and ends of the deal on the purchase. I will continue using MONEYME for any future purchases for the simple reason of not having to deal with all the issues the big banks have with a purchase. Great work Eujin.

LeslieSept 26, 2025

Super fast and easy application.

Excellent Customers service, super fast and easy application with the response within hrs.

ConsumerSep 18, 2025

Approval was fast and even the car dealership was blown away.

Approval was fast and even the car dealership was blown away by the speed and ease of dealing with MONEYME. I had my new car in no time! Highly recommend!

NicholeSep 13, 2025

MONEYME is one of the best finance companies I've ever gone through.

MONEYME is one of the best finance companies I've ever gone through great people and what a fantastic service they provide. MONEYME definitely goes above and beyond to satisfy their customers, thank you so much I would highly recommend MONEYME to anyone Australia wide.

TrinitySep 10, 2025

Great rate and helpful people making this purchase smooth and easy.

A fantastic experience of getting the right finance for my new vehicle. No fuss, no problems, a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

ShazJuly 10, 2025

Very Happy!! MONEYME finance was so easy to work with.

They made the whole experience from start to finish stress free and simple for me to understand which was exactly what I needed. They were just so quick and efficient, the only waiting was with the car yard itself. I would use MONEYME again. I highly recommend them to anyone wanting quick approval at a great rate with fantastic service.

BrookeMay 23, 2025

Overall great experience.

Super quick approval and great interest rate. Money was in the bank within minutes of me accepting the offer. Overall great experience.

JodieMay 9, 2025

Very easy, seamless process.

Every part of the way i had ongoing communication and I knew where I was at every stage. I was able to sign all documents online. The contract was easy to read and understand. The app is very easy to navigate with a easy to find phone number if i ever need assistance.

KerrinMay 21, 2025

Quick and easy to apply.

Great interest compared to other loans. No hidden costs. Fast and efficient.

RenayMar 7, 2025

A fantastic experience for getting the right finance from my new vehicle.

No fuss, no problems a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

ShazJun 8, 2025

Easiest process.

MONEYME has been so easy to navigate the website and the app, always in contact every step of the application. They gave me a chance to get my family a new car. Great company, fair prices, 100%

JadeJan 13, 2025

Great for debt consolidation!

I have used MONEYME a few times as they are simple and efficient. Response time is super quick and the rates are competitive. I was on a crazy rate with a credit card company and used MONEYME to consolidate that debt and reduce my repayments.

ECJan 6, 2025

Professional fast service.

We had a wonderful experience with MONEYME, fast service and very professional, we will definitely be using them again!

BiancaJan 03, 2025

Will definitely be recommending MONEYME to friends and family!

Quick and efficient service, will definitely be recommending MONEYME to friends and family!

JackOct 15, 2025

Quick, easy and hassle free!

Quick, easy and hassle free! I was pleasantly surprised how easy the process was. Also being able to make extra repayments and payout the loan early without penalty, is a big bonus. Recommended!

LindaSep 27, 2025

Easy to deal with.

Easy to deal with and open about the odds and ends of the deal on the purchase. I will continue using MONEYME for any future purchases for the simple reason of not having to deal with all the issues the big banks have with a purchase. Great work Eujin.

LeslieSept 26, 2025

Super fast and easy application.

Excellent Customers service, super fast and easy application with the response within hrs.

ConsumerSep 18, 2025

Approval was fast and even the car dealership was blown away.

Approval was fast and even the car dealership was blown away by the speed and ease of dealing with MONEYME. I had my new car in no time! Highly recommend!

NicholeSep 13, 2025

MONEYME is one of the best finance companies I've ever gone through.

MONEYME is one of the best finance companies I've ever gone through great people and what a fantastic service they provide. MONEYME definitely goes above and beyond to satisfy their customers, thank you so much I would highly recommend MONEYME to anyone Australia wide.

TrinitySep 10, 2025

Great rate and helpful people making this purchase smooth and easy.

A fantastic experience of getting the right finance for my new vehicle. No fuss, no problems, a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

ShazJuly 10, 2025

Very Happy!! MONEYME finance was so easy to work with.

They made the whole experience from start to finish stress free and simple for me to understand which was exactly what I needed. They were just so quick and efficient, the only waiting was with the car yard itself. I would use MONEYME again. I highly recommend them to anyone wanting quick approval at a great rate with fantastic service.

BrookeMay 23, 2025

Overall great experience.

Super quick approval and great interest rate. Money was in the bank within minutes of me accepting the offer. Overall great experience.

JodieMay 9, 2025

Very easy, seamless process.

Every part of the way i had ongoing communication and I knew where I was at every stage. I was able to sign all documents online. The contract was easy to read and understand. The app is very easy to navigate with a easy to find phone number if i ever need assistance.

KerrinMay 21, 2025

Quick and easy to apply.

Great interest compared to other loans. No hidden costs. Fast and efficient.

RenayMar 7, 2025

A fantastic experience for getting the right finance from my new vehicle.

No fuss, no problems a fast and easy solution with a great rate and helpful people making this purchase smooth and easy.

ShazJun 8, 2025

Easiest process.

MONEYME has been so easy to navigate the website and the app, always in contact every step of the application. They gave me a chance to get my family a new car. Great company, fair prices, 100%

JadeJan 13, 2025

Great for debt consolidation!

I have used MONEYME a few times as they are simple and efficient. Response time is super quick and the rates are competitive. I was on a crazy rate with a credit card company and used MONEYME to consolidate that debt and reduce my repayments.

ECJan 6, 2025

Professional fast service.

We had a wonderful experience with MONEYME, fast service and very professional, we will definitely be using them again!

BiancaJan 03, 2025

With no impact to your credit score

What is a credit score?

A credit score is a number that demonstrates your credit history and financial habits. Lenders use this score to assess your risk as a borrower and determine whether or not to lend you money, and if so, at what interest rate. A higher credit score generally indicates a lower risk to the lender, which can result in more favourable loan terms.

Why choose MONEYME to check your credit score?

Find out why so many Australians choose our app to build brighter financial futures.

All-in-one app: The MONEYME app makes it simple to perform a free credit score check in Australia and explore other products.

User-friendly: Forget financial jargon and confusing products. We make understanding your credit score easier than ever.

Personalised insights: Get more than just a score. Use our in-depth insights and actionable advice to boost your creditworthiness.

Trusted by thousands: Join thousands of Australians on the MONEYME app.

A sustainable choice: MONEYME is committed to using business as a force for good and meeting high social and environmental standards..

Check your score

for free

Checking won't impact your score, so what are you waiting for? Download the MONEYME app to check your score in seconds.

Won't impact your credit score!

Purpose-driven

and responsible

At MONEYME, we're not just here to provide low rate loans - we're here to make a difference. We believe in providing smart, responsible lending that keeps you financially on track, whilst doing good for the planet.

As a Certified B CorporationTM we're big on sustainability. We hold ourselves accountable to the high standards of the B Corp movement, supporting renewable energy projects, doing our part for the community, and striving towards a greener future.

Explore our impact

Supporting

World VisionWe sponsor a child on behalf of every Australian employee. All of these children live in the same community in Uganda, called Busakira.

Item 1 of 5

*Loan terms range from 3 to 7 years. Annual Percentage Rates (APR) from 6.24% p.a. (comparison rate from 6.95%). The maximum APR is 25.85% p.a. (27.24% p.a. comparison rate). Representative example: a loan of $30,000 over 5 years with an interest rate of 9.44% p.a. (10.82% p.a. comparison rate) would require monthly repayments of $649.56, with total repayments of $38,973.48, including a $495 establishment fee and a $10 monthly fee. Rates displayed are for customers with an excellent credit history. For other borrowers, an establishment fee of $395 or $495 will apply, based on loan amount. A $10 monthly fee applies to all personal loans.

WARNING: This comparison rate is true only for the example given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

MONEYME acknowledges Aboriginal and Torres Strait Islander peoples as the first people and Traditional Custodians of the land and waterways throughout Australia. We recognise their continued connection to culture, community and Country, and pay our respects to Elders past and present. Learn more about our commitment here.

Our business hours

Sydney/Melbourne time

Customers

Monday - Friday

8AM-7PM

Saturday

9AM-6PM

Sunday

Closed

Partners

Monday - Friday

8AM-5PM

Saturday & Sunday

9AM-3PM

Customer support

Copyright 2026 l MoneyMe Financial Group Pty Ltd l ABN 40 163 691 236 l Australian credit licence number 442218 | Credit criteria, fees, charges, terms and conditions apply.