*This comparison rate is based on an unsecured variable rate personal loan of $30,000 for a term of 5 years. Rates displayed are for customers with an excellent credit history, where a $0 establishment fee applies. For other borrowers, an establishment fee of $395 or $495 will apply, based on loan amount. A $10 monthly fee applies to all personal loans. WARNING: This comparison rate is true only for the example given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

Establishment fee

$0 - $395

Loans up to $15,000

$0 - $495

Loans above $15,001

Loan term

3 to 7 years

Our fees

$10

Monthly fee

$0

Early exit fees

*This comparison rate is based on an unsecured variable rate personal loan of $30,000 for a term of 5 years. Rates displayed are for customers with an excellent credit history, where a $0 establishment fee applies. For other borrowers, an establishment fee of $395 or $495 will apply, based on loan amount. A $10 monthly fee applies to all personal loans. WARNING: This comparison rate is true only for the example given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate.

Personal loan vs. Car Loan

Are you in the market for a new car and wondering whether you should get a personal loan vs car loan? Cars can be expensive, so in many cases, when you purchase a car you won’t be able to pay for it all upfront and will need car finance. There are several factors to consider when deciding between a personal loan and a car loan as there are pros and cons for both options.

What is the difference between a personal loan and a car loan?

Firstly, you may be wondering how a personal loan is different from a car loan. A car loan is a type of personal loan that is designed specifically to use when you are buying a car. A car loan is usually a secured loan, with the car you are buying serving as the collateral and it typically has a variable interest rate. If you shop around, you can find car loans that are unsecured or have variable interest rates but this isn’t as common. If you get a car loan with a variable rate, it’s easier to budget your repayments but there is less flexibility if you want to pay off your loan early. Using the car as security will mean you are likely to have a lower interest rate, and it also means the approval process will be easier if you don’t have a good credit history. You’ll need to be careful that you don’t skip any repayments though, as you don’t want to risk your vehicle being repossessed.

Personal loans are not restricted to only for buying a car. You can borrow money with a personal loan for many other purposes as well, such as unexpected bills, house renovations, booking a holiday, paying for a wedding and much more. You can even use personal loans for debt consolidation. Personal loans are very flexible – you can get secured or unsecured loans, variable interest rates and there is often flexibility in the payment structure. So whether you want short term loans or longer-term loans, you can choose a personal loan that best suits your financial situation or needs.

Know the option that suits you

Though every person’s situation is different, in many situations getting a debt consolidation loan can be a great idea to save you both time and money. For starters, it means you are less likely to skip a repayment as you will only have one monthly repayment to pay each month (or however often your payment loan terms are) so it will be easier to remember one regular repayment. In most cases, by consolidating your debts, you will probably end up paying less in loan repayments for this single loan than if you kept paying off all your debts separately. This is because instead of paying multiple loans with higher interest rates, you’ll be paying one loan that is likely to have a better rate. Plus, you would only need to pay one annual fee on your account.

Who offers debt consolidation loans?

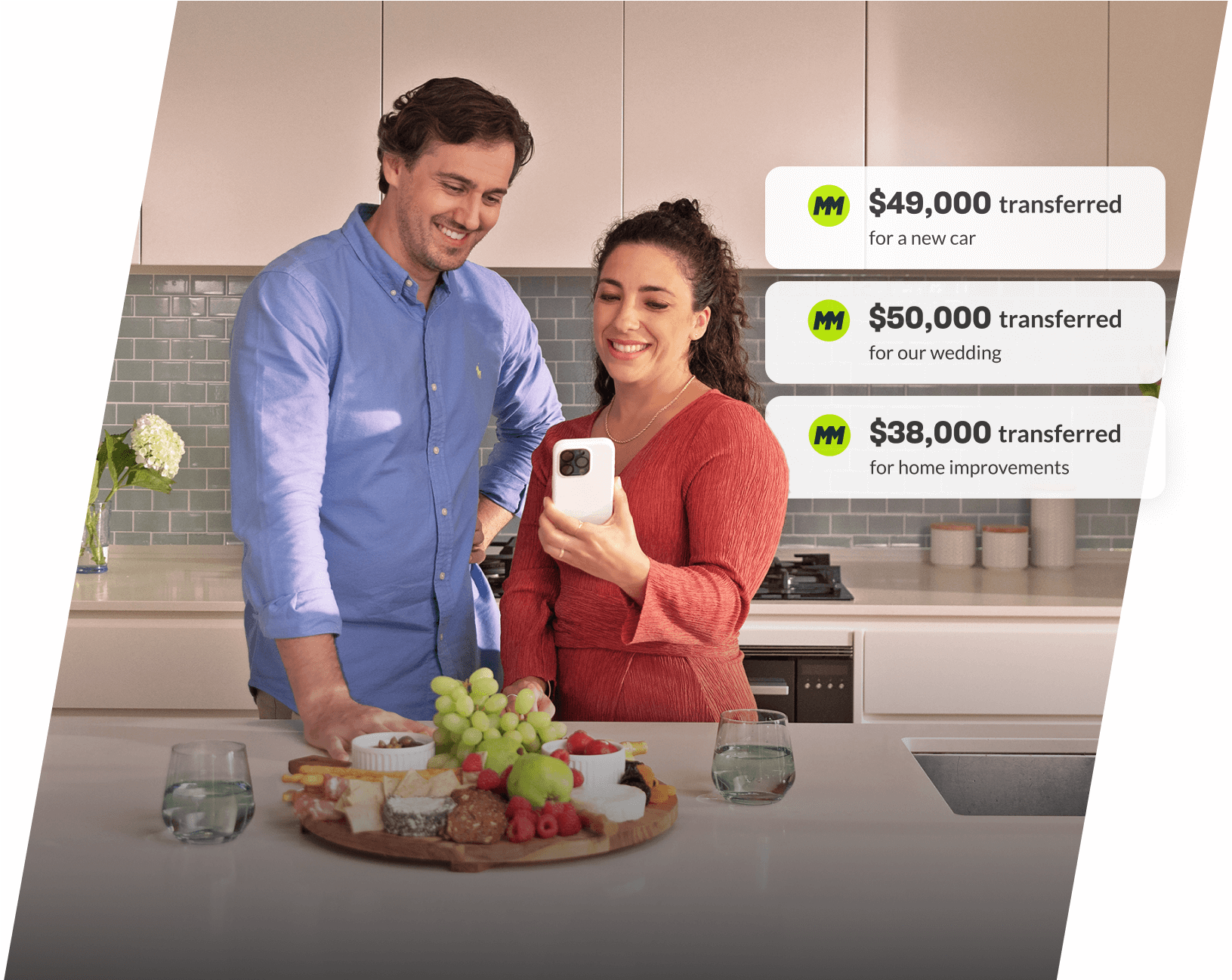

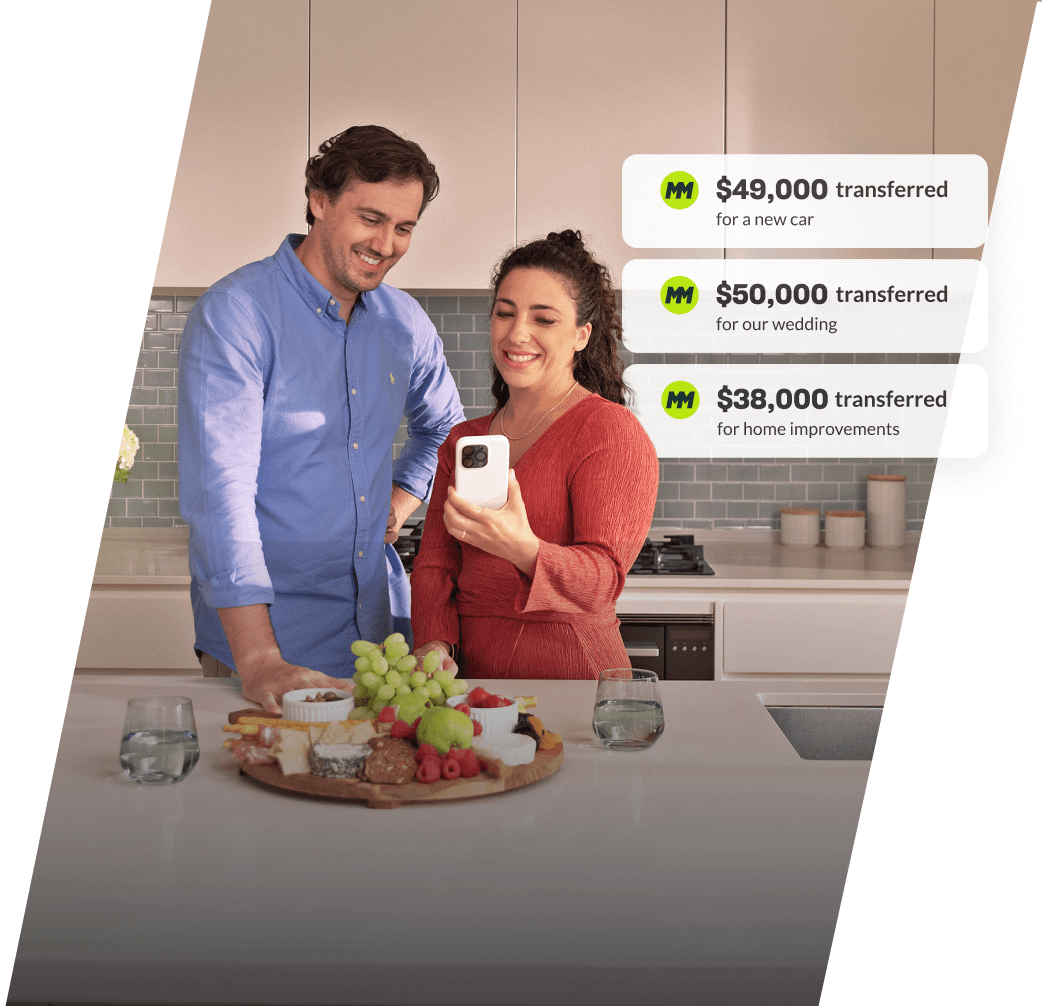

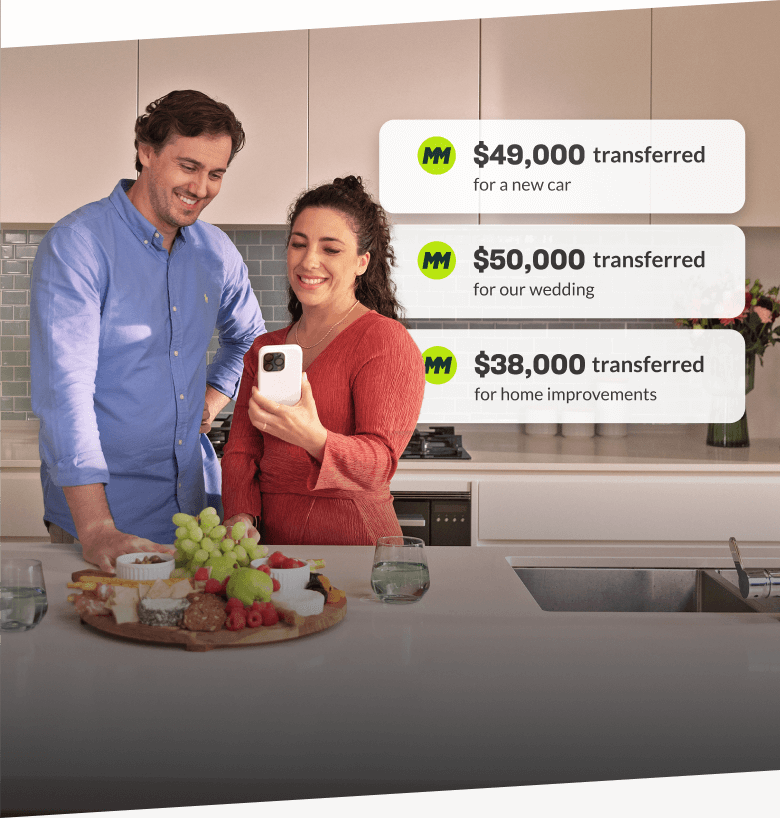

Traditionally, when looking at personal loan vs car loan, many customers opted for car loans when purchasing a car as it was convenient and fast. But in some cases, you may find a personal loan to be a better option, especially now with more online lenders. For example, credit providers such as MoneyMe offer personalloans online of up to $50,000. If you are taking out an unsecured personal loan from $5,000 to $50,000 you can choose a minimum repayment period of 12 months and a maximum of 60 months depending on the loan amount. It comes with a simple repayment plan and it costs you nothing to repay early. Low interest rates are tailored to your profile and you don’t need to fill out mountains of paperwork!

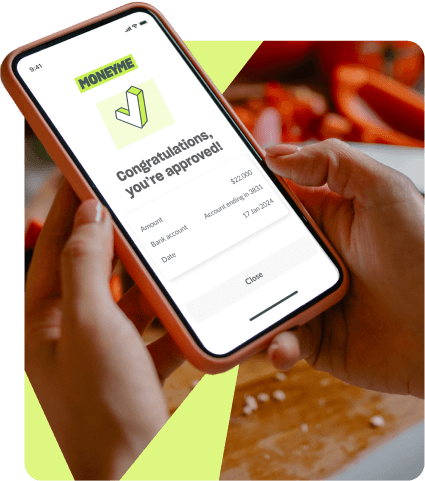

When you are buying a new or used car, you usually spend a lot of time researching and finding the best deal. So when you do find a good deal, you need to act quickly if you want to secure it. That’s where a MoneyMe unsecured car loan comes in. MoneyMeexpress loans can be approved online in minutes, and the cash can be in your account on the same day. Depending on who you bank with, with MoneyMe’s quick loans, the money can be in your account in minutes. There are advantages and disadvantages on a personal loan vs car loan, but if you want to be the owner of a new car sooner rather than later, MoneyMe can help! Apply online today for same-day loans of up to $50,000 and you could be driving away in your new car in no time!

To reset your passcode, please provide the

following details

The details you provided did not match our records

Can’t remember your details? Call us on 1300 669 059 and we’ll help you recover your account

Checking your details...

Scan QR code to download app

Check your score to WIN $1,000

Want to boost your financial wellness while also having a shot at winning some extra cash? Simply log into the MONEYME App and check your credit score every month to go in the draw to win $1,000!